Homeowners Insurance and Home Improvements_ Updating Your Coverage

Understanding Homeowners Insurance Basics

Homeowners insurance is a crucial safeguard for your most valuable asset your home. It protects you financially from unexpected events, such as fire, theft, vandalism, and certain natural disasters. Understanding the basics of homeowners insurance is essential for making informed decisions about your coverage needs.

A standard homeowners insurance policy typically includes four main types of coverage:

- Dwelling Coverage: This covers the physical structure of your home, including the walls, roof, and attached structures like a garage or deck.

- Personal Property Coverage: This covers your belongings inside the home, such as furniture, electronics, clothing, and appliances.

- Liability Coverage: This protects you financially if someone is injured on your property or if you accidentally damage someone else's property.

- Additional Living Expenses (ALE) Coverage: This covers the costs of temporary housing and other expenses if you are unable to live in your home due to a covered loss.

It's important to understand the different types of homeowners insurance policies available. The most common type is an HO-3 policy, which provides all-risk coverage for your dwelling and named-peril coverage for your personal property. Other types of policies, such as HO-5 (comprehensive coverage) and HO-8 (modified coverage), may be more suitable depending on your individual needs and circumstances.

Homeowners Insurance Coverage Options Explained

Beyond the basic coverage types, homeowners insurance policies offer a variety of optional coverages that can provide additional protection. Some common options include:

- Replacement Cost Coverage: This pays to replace your belongings with new items, regardless of their age or condition.

- Guaranteed Replacement Cost Coverage: This pays the full cost to rebuild your home, even if it exceeds your policy's coverage limit.

- Personal Injury Coverage: This protects you financially if you are sued for libel, slander, or other personal injury claims.

- Flood Insurance: This covers damage caused by flooding, which is typically not covered by standard homeowners insurance policies. (Offered through the National Flood Insurance Program - NFIP and private insurers)

- Earthquake Insurance: This covers damage caused by earthquakes, which is also typically not covered by standard homeowners insurance policies.

- Sewer Backup Coverage: This covers damage caused by sewer backups, which can be a common and costly problem.

- Identity Theft Protection: This helps you recover from identity theft by covering expenses such as legal fees and credit monitoring.

Choosing the right coverage options can provide peace of mind and protect you from significant financial losses. It's important to carefully consider your individual needs and risk tolerance when selecting your coverage options.

Factors Influencing Homeowners Insurance Premiums

Homeowners insurance premiums are determined by a variety of factors, including:

- Location: Homes in areas prone to natural disasters, such as hurricanes, tornadoes, or wildfires, typically have higher premiums.

- Home Value: The higher the value of your home, the higher your premiums will be.

- Coverage Amounts: Higher coverage limits result in higher premiums.

- Deductible: A higher deductible will lower your premiums, but it will also mean you have to pay more out of pocket if you file a claim.

- Claims History: If you have a history of filing claims, your premiums will likely be higher.

- Credit Score: In many states, insurance companies use credit scores to assess risk. A lower credit score may result in higher premiums.

- Home's Age and Condition: Older homes or homes in poor condition may have higher premiums due to the increased risk of damage.

- Security Features: Homes with security systems, smoke detectors, and other safety features may qualify for discounts.

Understanding these factors can help you take steps to lower your homeowners insurance premiums. For example, you can improve your credit score, increase your deductible, or install security features.

Comparing Homeowners Insurance Quotes and Finding the Best Policy

Shopping around and comparing quotes from different insurance companies is essential for finding the best homeowners insurance policy at the best price. Here's how to effectively compare quotes:

- Get Quotes from Multiple Insurers: Contact at least three to five different insurance companies or independent agents to get quotes.

- Compare Coverage Options: Make sure you are comparing the same coverage options and limits across all quotes.

- Consider the Deductible: Choose a deductible that you are comfortable paying out of pocket.

- Read the Fine Print: Carefully review the policy documents to understand the terms and conditions of coverage.

- Check the Insurer's Financial Strength: Choose an insurer with a strong financial rating from a reputable rating agency like A.M. Best or Standard & Poor's.

- Consider Customer Service: Read online reviews and check the insurer's customer service ratings to get an idea of their responsiveness and claims handling process.

Don't just focus on the price. Consider the overall value of the policy, including the coverage options, deductible, and customer service. A slightly more expensive policy with better coverage and customer service may be worth the extra cost.

Homeowners Insurance and Home Improvements Updating Your Coverage

Home improvements can significantly increase the value of your home, and it's essential to update your homeowners insurance coverage accordingly. Here's how to ensure you have adequate coverage after making home improvements:

- Reassess Your Coverage Needs: Determine the new replacement cost of your home after the improvements.

- Contact Your Insurance Company: Inform your insurance company about the home improvements and provide them with updated information about the value of your home.

- Increase Your Coverage Limits: Increase your dwelling coverage limits to reflect the increased value of your home.

- Consider Additional Coverage: If you've added new features to your home, such as a swimming pool or a home theater, you may need to add additional coverage to protect them.

- Document Your Improvements: Keep records of all home improvements, including receipts, contracts, and photos. This will be helpful if you ever need to file a claim.

Failing to update your homeowners insurance coverage after making home improvements can leave you underinsured and vulnerable to significant financial losses. It's better to be proactive and ensure you have adequate coverage.

Homeowners Insurance Claims Process Understanding What to Do

Filing a homeowners insurance claim can be a stressful experience, but understanding the process can make it easier. Here's a step-by-step guide to filing a claim:

- Report the Loss: Contact your insurance company as soon as possible after the loss occurs.

- Document the Damage: Take photos and videos of the damage to your home and belongings.

- Protect Your Property: Take steps to prevent further damage to your property, such as covering damaged roofs or boarding up broken windows.

- File a Police Report: If the loss was caused by theft or vandalism, file a police report.

- Complete a Claim Form: Your insurance company will provide you with a claim form to complete. Be sure to provide accurate and detailed information about the loss.

- Meet with an Adjuster: An insurance adjuster will be assigned to your claim. They will inspect the damage and estimate the cost of repairs.

- Review the Settlement Offer: Carefully review the settlement offer from your insurance company. If you disagree with the offer, you can negotiate with the adjuster.

- Get Repairs Done: Once you have agreed on a settlement, you can start getting repairs done.

Keep detailed records of all communication with your insurance company, as well as receipts for any expenses you incur as a result of the loss. If you have any questions or concerns, don't hesitate to contact your insurance company or a public adjuster.

Homeowners Insurance Discounts Save Money on Your Premiums

Many insurance companies offer discounts on homeowners insurance premiums. Here are some common discounts you may be eligible for:

- Multi-Policy Discount: Get a discount by bundling your homeowners insurance with other policies, such as auto insurance.

- Home Security System Discount: Get a discount by installing a home security system.

- Smoke Detector Discount: Get a discount by installing smoke detectors.

- Fire Alarm Discount: Get a discount by installing a fire alarm system.

- Sprinkler System Discount: Get a discount by installing a sprinkler system.

- New Home Discount: Get a discount if your home is newly built.

- Claims-Free Discount: Get a discount if you haven't filed any claims in the past few years.

- Senior Citizen Discount: Get a discount if you are a senior citizen.

- Military Discount: Get a discount if you are a member of the military.

- Roofing Material Discount: Get a discount if your roof is made of durable material (e.g., impact-resistant shingles).

Contact your insurance company to inquire about available discounts. You may be surprised at how much you can save on your premiums.

The Importance of Maintaining Your Home to Avoid Insurance Issues

Properly maintaining your home is crucial not only for its value and your comfort but also for avoiding potential insurance issues. Neglecting home maintenance can lead to uncovered damages and even policy cancellations. Here's why and how to maintain your home effectively:

- Preventing Damage: Regular maintenance can prevent small problems from becoming big, costly ones. For example, fixing a leaky roof promptly can prevent water damage to your walls and ceilings.

- Avoiding Claim Denials: Insurance companies may deny claims if the damage is due to negligence or lack of maintenance. For instance, they might deny a claim for mold damage if it's clear that a leak has been ignored for a long time.

- Maintaining Policy Coverage: Some insurance policies require you to maintain your home in good condition. Failure to do so could result in cancellation or non-renewal of your policy.

Here are some key areas to focus on for home maintenance:

- Roof: Inspect your roof regularly for missing or damaged shingles, leaks, and signs of wear and tear. Clean gutters and downspouts to prevent water buildup.

- Plumbing: Check for leaks under sinks, around toilets, and in your basement. Address plumbing issues promptly to prevent water damage and mold growth.

- Electrical System: Have your electrical system inspected periodically by a qualified electrician. Replace outdated wiring and address any electrical hazards.

- Heating and Cooling Systems: Schedule regular maintenance for your HVAC systems to ensure they are operating efficiently and safely.

- Exterior: Inspect your home's exterior for cracks, holes, and other signs of damage. Repair any damage promptly to prevent further deterioration.

- Landscaping: Keep trees and shrubs trimmed away from your home to prevent damage from falling branches and to reduce the risk of pests.

Understanding Homeowners Insurance Exclusions

Homeowners insurance policies typically have exclusions, which are events or perils that are not covered. It's important to understand these exclusions so you can take steps to protect yourself from uncovered losses. Common exclusions include:

- Flood: Flood damage is typically not covered by standard homeowners insurance policies. You will need to purchase a separate flood insurance policy.

- Earthquake: Earthquake damage is also typically not covered by standard homeowners insurance policies. You will need to purchase a separate earthquake insurance policy.

- Wear and Tear: Damage caused by normal wear and tear is not covered. This includes things like leaky faucets, cracked paint, and worn-out appliances.

- Pest Infestation: Damage caused by pests, such as termites, rodents, or insects, is typically not covered.

- Mold: Mold damage is often excluded or limited in coverage, especially if it's due to negligence or lack of maintenance.

- War: Damage caused by war is not covered.

- Nuclear Hazard: Damage caused by a nuclear hazard is not covered.

- Intentional Acts: Damage caused by intentional acts is not covered.

- Sewer Backup (without specific coverage): Standard policies often exclude sewer backup; adding specific coverage is often necessary.

Review your policy carefully to understand the exclusions. If you are concerned about any of these exclusions, you may be able to purchase additional coverage.

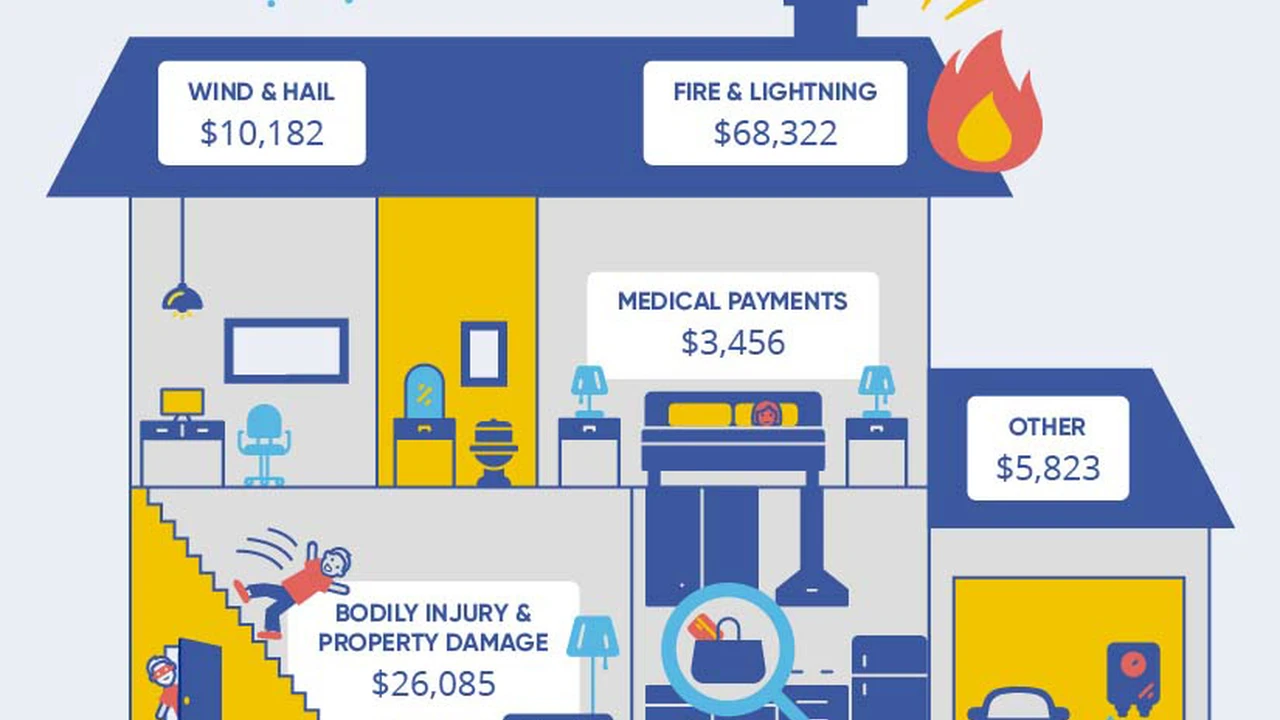

Homeowners Insurance and Natural Disasters Coverage Details

Homeowners insurance provides coverage for various natural disasters, but it's crucial to understand the specifics of what's covered and what's not. This section details coverage for common natural disasters:

- Fire: Fire is generally covered by homeowners insurance, including wildfires. Coverage extends to damage to the dwelling and personal property.

- Windstorm: Wind damage, including damage from hurricanes and tornadoes, is typically covered. However, some policies may have separate deductibles for windstorm damage.

- Hail: Hail damage to your roof, siding, and windows is usually covered.

- Lightning: Damage caused by lightning strikes is covered.

- Snow and Ice: Damage caused by the weight of snow and ice is generally covered, such as roof collapse or damage from ice dams.

- Water Damage (from burst pipes, etc.): Water damage from sudden and accidental events, such as burst pipes, is usually covered.

- Flood: As mentioned previously, flood damage is typically excluded and requires a separate flood insurance policy.

- Earthquake: Earthquake damage is also typically excluded and requires a separate earthquake insurance policy.

It's important to review your policy to understand the specific coverage limits and deductibles for each type of natural disaster. If you live in an area prone to certain natural disasters, you may need to purchase additional coverage or consider a policy with higher coverage limits.

Specific Product Recommendations for Homeowners Insurance

Choosing the right homeowners insurance can be overwhelming. Here are some product recommendations based on different needs and scenarios:

- For Comprehensive Coverage: Consider a policy from Chubb or Cincinnati Insurance. These companies are known for their comprehensive coverage options and excellent customer service. They often offer features like guaranteed replacement cost coverage and higher coverage limits for personal property.

- For Budget-Conscious Homeowners: Companies like Lemonade and Hippo offer competitive rates and user-friendly online platforms. Lemonade uses AI to streamline the claims process, while Hippo focuses on proactive home protection with smart home devices.

- For Coastal Properties: If you live in a coastal area prone to hurricanes, consider policies from companies like State Farm or Allstate. These companies have experience handling claims in coastal regions and offer specialized coverage options, such as windstorm coverage and flood insurance (in some cases, as an add-on or through NFIP).

- For High-Value Homes: For homes with significant value, consider policies from companies like PURE Insurance or AIG Private Client Group. These companies cater to high-net-worth individuals and offer customized coverage options, such as coverage for fine art, jewelry, and other valuable possessions. They also provide concierge-level customer service.

- For Renters: While not homeowners insurance, renters insurance is crucial. Companies like Progressive and Allstate offer affordable renters insurance policies that cover personal property, liability, and additional living expenses.

Example Use Cases:

- Chubb: A homeowner with a valuable art collection chooses Chubb for their comprehensive coverage of personal property and specialized art insurance options.

- Lemonade: A young professional looking for an affordable and easy-to-use insurance option chooses Lemonade for their AI-powered claims process and low premiums.

- State Farm: A homeowner in Florida chooses State Farm for their experience handling hurricane claims and their comprehensive windstorm coverage.

- PURE Insurance: A homeowner with a high-value home and multiple properties chooses PURE Insurance for their customized coverage options and concierge-level service.

Homeowners Insurance Product Comparisons Detailed Information and Pricing

Here's a detailed comparison of some popular homeowners insurance products, including pricing information:

1. Chubb Homeowners Insurance:

- Coverage: Comprehensive coverage, including guaranteed replacement cost, high limits for personal property, and specialized coverage options for art and jewelry.

- Features: Risk consulting services, loss prevention resources, and concierge-level customer service.

- Pricing: Generally more expensive than other options, reflecting the higher level of coverage and service. Expect to pay at least $1,500 to $3,000+ per year for a home valued at $500,000, depending on location and specific coverage needs.

- Pros: Excellent coverage, top-notch customer service, and risk management resources.

- Cons: Higher premiums compared to other options.

2. Lemonade Homeowners Insurance:

- Coverage: Standard coverage, including dwelling, personal property, liability, and additional living expenses.

- Features: AI-powered claims process, user-friendly mobile app, and charitable giveback program.

- Pricing: Competitive rates, often lower than traditional insurers. Expect to pay around $800 to $1,500 per year for a home valued at $500,000, depending on location and specific coverage needs.

- Pros: Affordable premiums, easy-to-use platform, and fast claims processing.

- Cons: Coverage options may be more limited compared to Chubb or Cincinnati Insurance.

3. State Farm Homeowners Insurance:

- Coverage: Broad coverage options, including dwelling, personal property, liability, and additional living expenses. Offers options for Guaranteed Replacement Cost and increased limits.

- Features: Local agent support, strong financial stability, and a wide range of discounts.

- Pricing: Mid-range pricing, generally competitive with other traditional insurers. Expect to pay around $1,000 to $2,000 per year for a home valued at $500,000, depending on location and specific coverage needs.

- Pros: Strong reputation, wide availability, and local agent support.

- Cons: Claims process can sometimes be slower compared to Lemonade or Hippo.

4. Hippo Homeowners Insurance:

- Coverage: Standard coverage, with options for smart home device integration and proactive home protection.

- Features: Smart home device discounts, proactive home monitoring, and fast claims processing.

- Pricing: Competitive rates, often lower than traditional insurers. Expect to pay around $900 to $1,800 per year for a home valued at $500,000, depending on location and specific coverage needs.

- Pros: Affordable premiums, smart home device integration, and proactive home protection.

- Cons: Coverage options may be more limited compared to Chubb or Cincinnati Insurance. Focuses heavily on technology, which might not appeal to everyone.

Disclaimer: These prices are estimates and may vary depending on your individual circumstances. It's always best to get a personalized quote from each insurance company to determine the actual cost of coverage.

Frequently Asked Questions About Homeowners Insurance

Here are some frequently asked questions about homeowners insurance:

- How much homeowners insurance do I need? You need enough coverage to rebuild your home and replace your belongings if they are destroyed. Consult with an insurance agent to determine the appropriate coverage limits for your needs.

- What is the difference between replacement cost and actual cash value? Replacement cost pays to replace your belongings with new items, while actual cash value pays the depreciated value of your belongings. Replacement cost is generally recommended.

- What is a deductible? A deductible is the amount you pay out of pocket before your insurance company pays for a claim. A higher deductible will lower your premiums, but it will also mean you have to pay more if you file a claim.

- How can I lower my homeowners insurance premiums? You can lower your premiums by increasing your deductible, improving your credit score, installing security features, and shopping around for quotes.

- What should I do if I have a claim? Report the loss to your insurance company as soon as possible, document the damage, and protect your property from further damage.

Final Thoughts on Selecting the Right Homeowners Insurance

Choosing the right homeowners insurance is a significant decision that requires careful consideration. By understanding the basics of homeowners insurance, comparing coverage options, and shopping around for quotes, you can find a policy that provides adequate protection and peace of mind. Remember to review your policy regularly and update your coverage as needed to ensure you are always properly insured. Don't hesitate to consult with an insurance professional to get personalized advice and guidance.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)